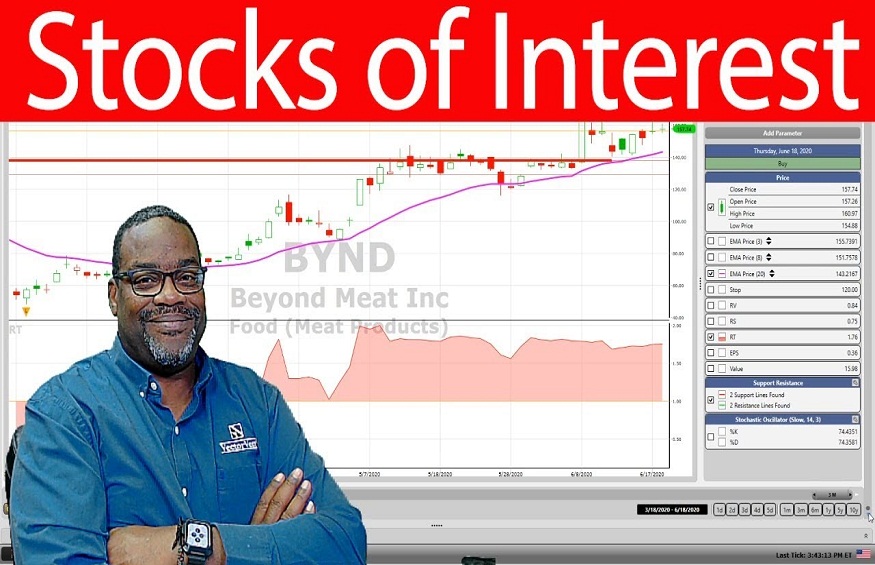

The comparative ranking record (RSI) has been transferred to the already category with a perusal of 76.49, but the BYND remains in a bullish uptrend. Traders should foresee a near-term union between that and a $160.00 booster and a $200.00 resistance range. Unless the company expects out, dealers will see a change to $240.00 values. Beyond Meat agreements ended up going even significantly greater in the middle of Thursday’s conference. The past eating Frankfurter Joins hits rackets all around the world. The stock has moved to the extremely crowded field, but the transforming normal dissimilarity (MACD) remains in a booming overall increase. Beyond Meats, Inc. (BYND stock) bids fell almost 20% in the middle of Tuesday’s meeting. Investigator Insight Goldman lowered the stock from Overweight to Impartial, but raised the cost goal from $120 to $121 a share. The company’s roll-out of Past Burger to basic needs stores around the country may face competition from comparable plant-based meat choices.

Authentication Of BYND

The company’s ambitious, smarter launch with a portion of the budget is forecast to extend to $210 million with a neutral EBITDA breakeven point. Assessors were positive about the manufacturer’s future growth. Dealers should wait a step to the trend line bolster for around $120.00 in the next sessions. The disproportionate rating list (RSI) forced 67.40 out of the excessively environment, while the expanding norm merging disparity (MACD) started to level down. Sales declined significantly in the last century. Customers have long been “cooler stacking,” or commonly affected to ensure that they have access to food bounty. Sales declined as they were 2.7%, equivalent to 69% at the time.

Beyond Meat promises, the driving force motivating greenhouse meat substitutes, grew by 65.3 per cent in 2020. The S&P 500 file delivered 18.4% for the final year. Further than the Meat’s stock finished in 2021 with a slight pick-up of 2.6 percent on Friday morning.The Route predicted a mistake of $0.06 per share. Sales rose 69% year-on-year to $113.3 million in the second quarter. This quarter was the main quarter that was fully influenced by generalized purchases.

In Q2, the rapid tailwind of BYND Meat’s supermarket offers was widespread as customers expanded their home-based food and supplied their refrigerators. The U.S. and foreign sales networks grew by 195 per cent and by 167 per cent on a stand-alone basis. Food benefits in both districts dropped by 61% and 57% week though.Beyond Meat has not reported the date of its fourth quarter discharge, but it is scheduled to be released at the end of February. Removable tray Road is now modeling revenue for the year to grow by 8 percent year-on-year. If you want to know more, you can check at https://www.webull.com/newslist/nasdaq-bynd.